| Alphabet builds AI moat with custom TPUs |

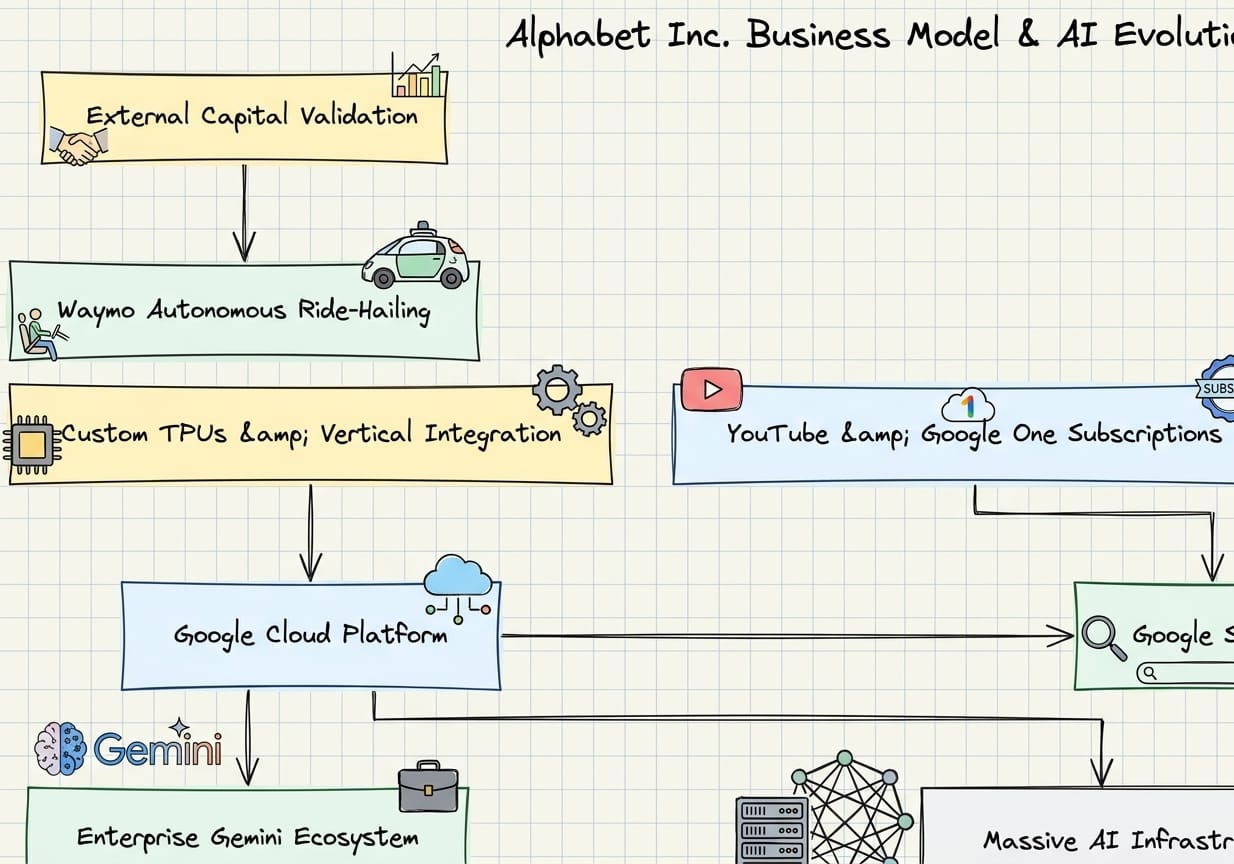

For over two decades, Alphabet has served as the primary gateway to the internet, leveraging a zero marginal cost distribution model to build the most lucrative advertising monopoly in history. However, the emergence of generative artificial intelligence has forced a fundamental re-architecture of this economic engine. The central question facing the company is no longer whether it can maintain its search market share, but whether it can successfully transition from being a distributor of third party links to a high capital intensity provider of synthesized intelligence. This shift represents a move from an asset light media aggregator to a vertically integrated infrastructure powerhouse. While the market often perceives this transition as a terminal threat to Alphabet’s value, the company is actually building a more durable, supply side moat rooted in custom silicon and proprietary compute economics.

This transition matters now because it marks the end of the legacy internet era and the beginning of the agentic AI era. Over the next decade, the battle for digital attention will be won by the firms that can manage the unit economics of AI inference at a global scale. Alphabet holds a distinct advantage here through its decade long investment in Tensor Processing Units. While competitors rely on expensive third party hardware, Alphabet’s vertical integration allows it to absorb the rising costs of AI synthesis more effectively than its peers. The core Google Services segment, anchored by Search and YouTube, continues to provide the immense liquidity required to fund this generational capital expenditure cycle. This funding and building dynamic allows the company to defend its search moat while simultaneously scaling Google Cloud and long dated optionality like Waymo into self sustaining pillars of value.

Despite these structural strengths, the market continues to price Alphabet at a discount, reflecting fears of regulatory intervention and margin compression. To navigate the next decade, investors must distinguish between the erosion of legacy distribution moats and the emergence of new, infrastructure based advantages. Key drivers to watch include the decoupling of revenue growth from traffic acquisition costs, the expansion of operating margins within Google Cloud, and the impact of regulatory remedies on default search agreements. Alphabet is currently executing a high stakes pivot that trades near term free cash flow for long term dominance in computational utility. If the company can maintain its auction density while lowering the cost of AI delivered answers, it will not only survive the disruption of search but will redefine the economics of information retrieval for the next generation.

| Company Overview & Business Model |

Alphabet Inc. operates as the premier global utility for information retrieval, digital attention, and computational infrastructure. While consensus often simplifies the entity into a mature digital advertising monopoly facing terminal decline from generative AI, a rigorous analysis of its business model reveals a more durable, mechanism-driven transition: the evolution from a zero-marginal-cost distributor of links to a high-capital-intensity provider of synthesized intelligence. The company’s financial architecture is shifting from a pure media aggregator, monetizing attention via auctions, to a hybrid ecosystem monetizing compute, productivity, and subscription-based utility.

| Source: P&L Post |

| The Core Economic Engine: Google Services |

The foundational cash generator remains Google Services, which produced $87.1 billion in revenue during the third quarter of 2025 Google Services revenue. This segment encompasses the core Search engine, YouTube, Android, Chrome, and hardware. The economic mechanism here is the auction of intent. By capturing high-fidelity user intent through Search and high-engagement attention through YouTube, Alphabet facilitates a real-time marketplace where advertisers bid for conversions.

Contrary to the "death of search" narrative, query volumes and commercial intensity have shown resilience. The integration of AI Overviews and multimodal capabilities has expanded the surface area for queries, rather than cannibalizing them. The durability of this model rests on a specific causal chain: user trust drives query volume, query volume drives auction density, and auction density drives pricing power. In Q3 2025, Search & other revenues grew 15% year-over-year to $56.6 billion, validating that AI-enhanced results are sustaining user engagement rather than displacing it Search revenue growth.

Within Services, YouTube has evolved into a dual-engine asset. It monetizes distinct attention economies: long-form "lean-back" consumption (TV screens) and short-form "lean-forward" engagement (Shorts). A critical inflexion point occurred in late 2025 when YouTube Shorts achieved revenue parity with traditional in-stream video on a per-watch-hour basis in the US Shorts monetization parity. This closes a significant arbitrage gap where engagement had previously outpaced monetization. Furthermore, the "Subscriptions, Platforms, and Devices" line item, often overlooked, has become a formidable recurring revenue stream, growing 21% to $12.9 billion subscription segment growth. With over 300 million paid subscriptions across YouTube Premium, Music, and Google One, Alphabet is successfully hedging its ad-cyclicality exposure with high-margin recurring cash flows paid subscription milestone.

| The Growth Engine: Google Cloud & AI Infrastructure |

Google Cloud has transitioned from a loss-leading challenger to a highly profitable, structural growth engine. The business model here differs fundamentally from Services; it is a consumption-based utility model where customers pay for compute, storage, and increasingly, API calls for generative AI models. In the third quarter of 2025, Cloud revenue accelerated 34% to $15.2 billion Cloud revenue acceleration.

Crucially, the operating leverage in this segment is beginning to materialize. Operating margins expanded significantly to 23.7%, up from 17.1% the prior year, demonstrating that the heavy upfront infrastructure costs are now being amortized over a wider revenue base Cloud margin expansion. The mechanism driving this is the "full-stack" AI advantage. Unlike competitors who must pay a "tax" to hardware providers like Nvidia for every chip, Alphabet’s decade-long investment in custom Tensor Processing Units (TPUs) allows it to offer AI training and inference at a structurally lower cost basis. This vertical integration is not merely a technical detail but a financial moat, enabling aggressive pricing while maintaining margins.

The demand signal is robust, evidenced by a backlog that swelled to $155 billion, up 82% year-over-year Cloud backlog growth. This metric provides high visibility into future revenue and suggests that enterprise adoption of the Gemini ecosystem is accelerating, with 7 billion tokens processed per minute via direct API use Gemini token volume.

| The Optionality Engine: Other Bets & Waymo |

For years, the "Other Bets" segment was viewed by investors as a tax on profitability, a collection of science projects with indefinite timelines. This view is now obsolete. The maturation of Waymo represents a tangible validation of Alphabet’s long-term capital allocation strategy. Waymo has successfully scaled its autonomous ride-hailing operations to over 15 million annualized rides, operating commercially in major metros like Phoenix, San Francisco, and Los Angeles Waymo ride volume.

The financial implications of Waymo’s recent $16 billion funding round, which valued the entity at $126 billion, are profound Waymo valuation. This external validation unlocks significant sum-of-the-parts value that was previously ascribed zero or negative value by public markets. While Other Bets still posted an operating loss of $1.4 billion in Q3 2025 Other Bets operating loss, the unit economics of autonomous transport are shifting from R&D expense to capital expansion. The business model for Waymo, Transportation as a Service (TaaS), promises higher terminal margins than traditional ride-hailing due to the elimination of driver labor costs, provided that vehicle utilization rates remain high to offset depreciation.

| Capital Allocation and The Cost Structure Shift |

Understanding Alphabet’s business model requires analyzing its changing cost structure. The primary lever for profitability is shifting from Traffic Acquisition Costs (TAC) to Capital Expenditures (CapEx). Historically, Alphabet paid billions to partners like Apple to secure distribution (TAC). While TAC remains significant at $14.9 billion for the quarter Traffic Acquisition Costs, the new imperative is the massive capital outlay required for AI infrastructure. The company raised its 2025 CapEx guidance to a range of $91-93 billion 2025 CapEx guidance.

This massive reinvestment creates a formidable barrier to entry. Only a handful of entities globally can fund ~$90 billion in annual infrastructure spend. This converts Alphabet’s cash flow from a return of capital mechanism into a defensive moat builder. The risk, however, is execution: if the returns on AI capital (ROAIC) fail to materialize in the form of higher ad pricing or cloud consumption, shareholder value destruction could be immense. However, early indicators, such as the 650 million monthly active users on the Gemini app, suggest that this infrastructure is successfully driving user adoption Gemini user base.

In summary, Alphabet is no longer just an ad-supported search engine. It is a diversified technology conglomerate where the high-margin cash flows from Search fund the capital-intensive build-out of the world's largest AI compute utility (Cloud) and the commercialization of frontier technologies (Waymo). The synergy between proprietary data (YouTube/Search), proprietary silicon (TPUs), and massive distribution (Android/Chrome) creates a self-reinforcing flywheel that is structurally difficult to disrupt, even in an AI-first world.

| Sources of Competitive Advantage |

Alphabet’s investment thesis has historically rested on a singular, self-reinforcing flywheel: the world’s most comprehensive index monetized through the world’s most efficient auction (Google Ads), protected by unparalleled distribution. However, the rise of generative AI and the shifting regulatory landscape have fundamentally altered the mechanism of this advantage. The company’s durability no longer relies solely on demand-side network effects (more searches = better results); it now increasingly depends on supply-side infrastructure economics and proprietary multimodal data. Investors must distinguish between the legacy moats that are currently eroding and the structural infrastructure advantages that competitors, including Microsoft and OpenAI, cannot easily replicate.

| The Silicon Moat: Vertical Integration and Cost Structures |

The most underappreciated structural advantage Alphabet possesses is its decade-long head start in custom silicon. While the consensus views the AI arms race as a battle for Nvidia GPUs, Alphabet operates a distinct economic model through its Tensor Processing Units (TPUs). This is not merely a technical detail; it is a critical margin defense mechanism. By designing chips in-house since 2015, Google avoids the gross margin stacking inherent in buying hardware from Nvidia.

The divergence in cost structures is significant. Analysis suggests that while Nvidia’s H100 and Blackwell GPUs offer raw performance leadership for general-purpose training, Google’s TPUs provide superior unit economics for sustained, hyperscale workloads. For specific internal workloads like search ranking and Gemini model training, TPUs can deliver significantly higher performance per dollar compared to merchant silicon. Google’s sixth-generation TPU, Trillium, and the subsequent TPU v7 (Ironwood) demonstrate this trajectory. The TPU v7 matches Nvidia’s Blackwell B200 in memory capacity at 192GB per chip but utilizes optical circuit switches (OCS) to reduce power conversion overhead, resulting in a reported 100% improvement in performance per watt over the previous generation TPU v7 Ironwood efficiency.

This vertical integration creates a "cost moat." As AI models scale, the primary constraint shifts from algorithm quality to inference cost. If Google can serve a query on Gemini for 30-50% lower cost than a competitor relying on Nvidia hardware (due to bypassing the hardware vendor’s margin and optimizing the entire stack from chip to compiler), it retains pricing power. This allows Alphabet to defend search margins even as the search interface shifts from 10-blue-links to computationally expensive generative answers.

| The Data Fortress: YouTube and Multimodal Training |

In the Large Language Model (LLM) era, text data has become commoditized; the Common Crawl is available to any well-funded startup. Alphabet’s enduring advantage lies in its proprietary, multimodal corpus, specifically YouTube. The platform dominates the attention economy, accounting for the greatest share of total social media time spent globally YouTube usage share.

This dominance translates directly into AI capability. Training state-of-the-art models requires vast amounts of video and audio data to understand causal reasoning, physical dynamics, and human dialogue nuances that text cannot convey. Reports indicate that Google utilized millions of YouTube video transcripts to train its Gemini models, a data source that is effectively closed off to competitors like OpenAI and Anthropic without significant legal risk or licensing friction Gemini training on YouTube data.

Competitors cannot easily replicate this asset. While they can scrape the open web, they cannot replicate the repository of user-generated video content that grows by thousands of hours every minute. This feedback loop, users uploading content that trains the models, which then power better tools to create content, creates a barrier to entry for "pure play" AI model builders who lack a consumer platform.

| Distribution: From Contractual Lock-in to Owned Real Estate |

The durability of Google Search’s market share, historically hovering above 90%, is currently facing its most severe stress test due to antitrust intervention. The Department of Justice’s victory in the search distribution case explicitly targets the exclusive contracts that cemented Google as the default engine on Apple devices and third-party browsers antitrust remedies ruling. The ruling prohibits Google from maintaining exclusive contracts for search distribution, dismantling a key defensive wall that cost the company billions annually in Traffic Acquisition Costs (TAC) but guaranteed volume.

However, the consensus view often overestimates the fragility of this position. Even without exclusive contracts, Alphabet retains massive "owned" distribution through Android and Chrome. Android holds over 70% of the global mobile operating system market Android global market share, and Chrome maintains a commanding 65%+ share of the desktop browser market Chrome desktop market share.

This "owned real estate" acts as a secondary moat. While the company may lose the automatic default on iOS, its control over the most widely used browser and mobile OS provides a buffer that pure software competitors lack. The integration of Gemini directly into Android and Chrome (e.g., "Circle to Search") attempts to bypass the browser address bar entirely, shifting the battleground from "default search engine" to "OS-level AI assistant." This transition is risky but leverages assets, specifically the 3.9 billion active Android devices, that are impossible for Microsoft or OpenAI to replicate without their own mobile hardware ecosystem Android user base scale.

| Financial Optionality and Capital Intensity |

The final structural advantage is financial scale acting as a filter. The transition to AI-first computing requires capital expenditures of unprecedented magnitude. Alphabet expects to invest approximately $75 billion in CapEx in 2025 alone, primarily for technical infrastructure 2025 CapEx guidance. This level of spending is prohibitive for virtually all competitors except Microsoft and Amazon.

This capital intensity protects incumbents. It transforms the market from one disrupted by garage startups to one dominated by industrial-scale compute utilities. Alphabet’s ability to fund this expansion internally through its core advertising business, which generated over $350 billion in revenue in 2024, allows it to weather the high efficiency-ramp period of AI adoption without reliance on external capital markets 2024 total revenue. The cash-rich balance sheet provides optionality to acquire talent, subsidize ecosystem adoption (via Google Cloud credits), and endure pricing wars that would bankrupt smaller model providers.

| Financial Engine & Unit Economics |

Alphabet operates one of the most efficient cash-generating machines in modern financial history, characterized by an aggressive transition from an asset-light advertising utility to a capital-intensive infrastructure conglomerate. The company's financial architecture is currently defined by a "funding-and-building" dynamic: the high-margin, mature Search and YouTube businesses provide the immense liquidity required to underwrite the generational capital expenditure cycle needed for Artificial Intelligence (AI) and Cloud supremacy.

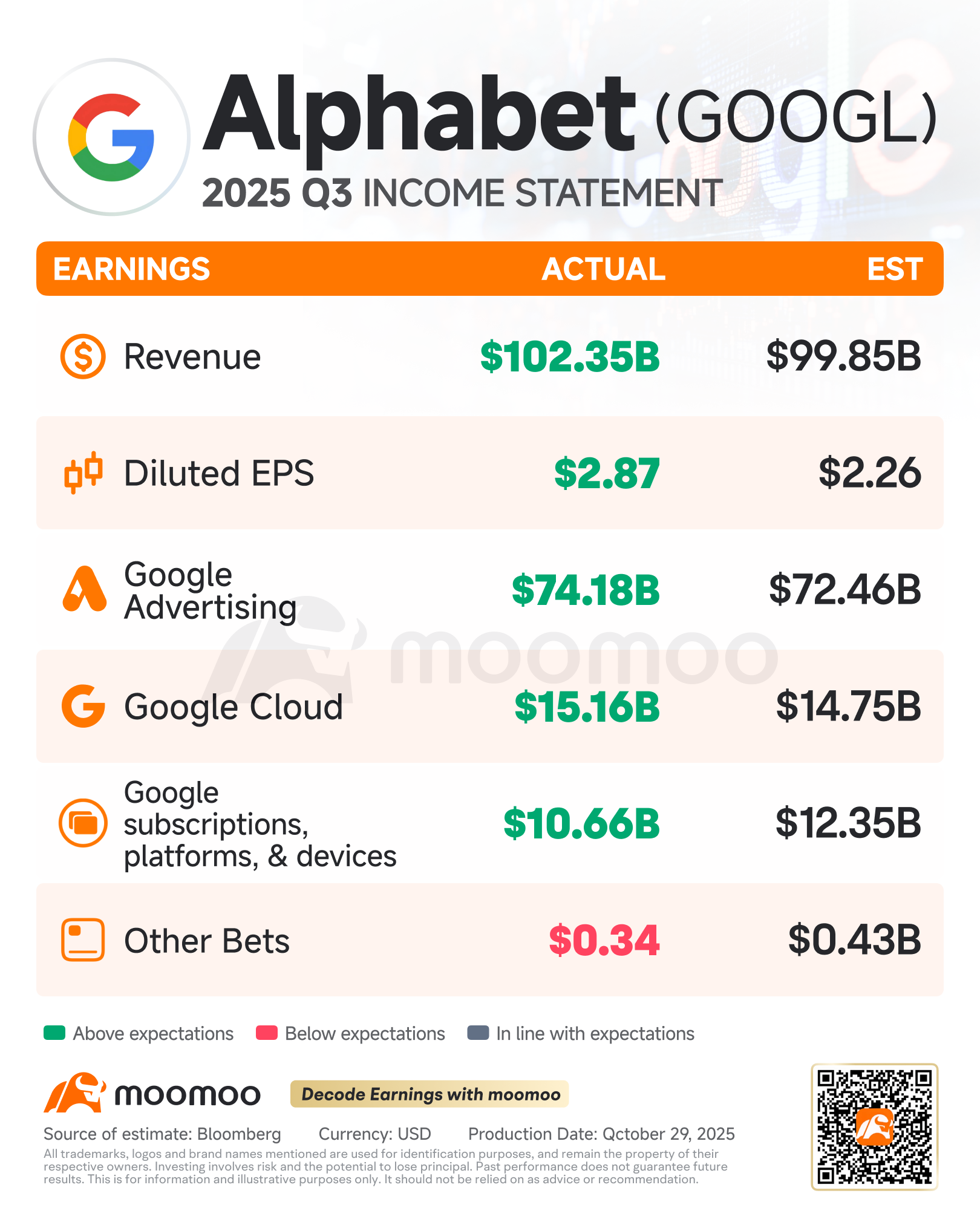

| Alphabet's Q3 2025 income statement shows consolidated revenue of $102.35B and strong performance across key segments like Google Advertising and Google Cloud. (Moomoo) |

| The Core Cash Generator: Search and Operating Leverage |

The durability of Alphabet’s valuation relies on the continued decoupling of revenue growth from traffic acquisition costs (TAC). Despite fears of AI disruption, the core search business demonstrates robust unit economics. In the third quarter of 2025, consolidated revenues accelerated to $102.3 billion, a 16% year-over-year increase consolidated revenues. Crucially, the cost of revenue structure exhibits positive operating leverage; while top-line revenue grew by double digits, TAC increased by only 8% to $14.9 billion TAC growth.

This divergence, where revenue growth outpaces the costs paid to distribution partners (like Apple and OEMs), signals that Alphabet retains pricing power and user loyalty even as search behaviors evolve. The company has successfully integrated AI Overviews without cannibalizing its monetization engine, as evidenced by Search & Other revenues climbing 15% to $56.6 billion Search segment revenue. By maintaining a disciplined TAC ratio relative to revenue, Alphabet preserves the gross margin capacity necessary to absorb the higher compute costs associated with generative AI queries.

| Cloud: The Unit Economics of Scale |

Google Cloud has transitioned from a margin-dilutive growth bet to a primary driver of operating profit expansion. The unit economics of the cloud business improve non-linearly with scale, as fixed infrastructure costs are amortized over a growing customer base. Google Cloud revenues surged 34% to $15.2 billion in Q3 2025 Google Cloud revenue. More importantly, the segment has achieved a distinct inflection point in profitability, delivering $3.6 billion in operating income Cloud operating income.

This profitability is underpinned by a massive backlog of $155 billion, which grew 46% sequentially Cloud backlog. This backlog provides high visibility into future cash flows, suggesting that the "land grab" phase of cloud infrastructure is converting into a recurring revenue annuity. The margin expansion in Cloud, reaching nearly 23.7% implies that Alphabet is successfully passing on the premium costs of AI compute to enterprise customers, neutralizing the impact of hardware depreciation.

| Capital Intensity and the AI Infrastructure Cycle |

The most significant structural shift in Alphabet's financial profile is the explosion in capital intensity. The company has moved away from the era of incremental server additions to a phase of massive, upfront infrastructure deployment. Management raised the 2025 capital expenditure guidance to a range of $91 billion to $93 billion 2025 CapEx guidance. This figure represents a dramatic escalation from the roughly $32 billion average annual spend observed between 2020 and 2023 historical capital expenditures.

This capital deployment creates a dual pressure on the financial statements. First, it suppresses free cash flow conversion in the near term, although operating cash flow remains robust enough to support it. Second, it creates a "depreciation shadow" that will drag on GAAP operating margins in future periods. Depreciation expenses surged 41% year-over-year in Q3 2025 depreciation expense growth. Investors must distinguish between this non-cash accounting drag and the actual health of the business; the rising depreciation confirms that Alphabet is aggressively refreshing its fleet with expensive, short-lived AI accelerators (GPUs and TPUs) to defend its technological moat.

| Cash Flow Resilience and Balance Sheet Fortification |

Despite the unprecedented capital outlays, Alphabet’s cash generation engine remains unbroken. The company generated $24.5 billion in free cash flow in Q3 2025 alone, contributing to a trailing 12-month free cash flow of $73.6 billion free cash flow. This internal liquidity allows Alphabet to fund its AI transformation entirely through operations, avoiding the debt markets that constrain smaller competitors.

The balance sheet remains a strategic fortress, holding $98.5 billion in cash and marketable securities cash balance. This liquidity provides immense optionality, allowing for continued shareholder returns via buybacks and dividends, declared at $0.21 per share dividend declaration, while simultaneously financing the largest infrastructure build-out in the company's history. The primary financial risk is not insolvency or liquidity, but rather the Return on Invested Capital (ROIC). With CapEx scaling faster than revenue, ROIC has compressed to approximately 26.8% ROIC metrics. The thesis for long-term value creation rests on the assumption that these massive upfront investments will yield high-margin returns through AI-integrated Search and Cloud services in the 2026–2028 timeframe.

| Strategy, Execution & Optionality |

Alphabet is currently executing a high-stakes structural pivot, transitioning its core mechanism of value capture from traffic distribution (the "ten blue links" era) to compute-intensive synthesis (the generative AI era). This shift is not merely a product update but a fundamental re-architecture of the company’s economic engine, necessitated by the rise of agentic AI and intensified by regulatory pressure. The thesis for long-term durability rests on three pillars: the aggressive capitalization of "full stack" AI infrastructure to defend the Search moat, the operationalization of efficiency through internal tooling (Project EAT), and the maturation of long-dated optionality (Waymo and Isomorphic Labs) into distinct valuation pillars.

| Multiple rows of Google's custom-designed TPU v5p pods are networked together within a data center. Google significantly increased its 2025 capital expenditure to expand technical infrastructure like these servers to support AI workloads. (Data Center Dynamics) |

| The Capital Intensity and Efficiency Paradox |

The company’s strategic priority is securing a dominant position in AI infrastructure, effectively trading near-term free cash flow for long-term terminal value defense. This is evident in the company's massive capital deployment, with 2025 capital expenditures revised upward to a range of $91 billion to $93 billion 2025 capital expenditure guidance. This spending is primarily directed toward technical infrastructure, servers, data centers, and TPUs, to support the voracious compute demands of Gemini models and Google Cloud’s expanding backlog.

Ideally, such massive capital intensity would compress margins. However, management is offsetting this through a rigorous internal mandate known as "Project EAT" (Eat your own dog food). This initiative aims to transform Google into a fully AI-powered workplace, using internal AI tools to automate workflows, optimize data center cooling, and streamline software development Project EAT efficiency initiative. This mechanism, using proprietary AI to reduce the marginal cost of producing AI, is critical. It explains how Alphabet maintained a 32% operating margin in Q4 2024 despite rising depreciation and infrastructure costs Q4 2024 operating margin. By Q3 2025, operating margins (excluding one-off fines) reached 33.9%, demonstrating that the company can decouple revenue growth from headcount growth via AI-driven operating leverage Q3 2025 operating margin.

| Defensive Strategy: Search Evolution and Antitrust |

The core Search business faces a dual threat: technological disruption from generative answers and regulatory dismantling. Strategically, Alphabet has chosen to cannibalize its own organic click-through rates (CTR) to retain user attention. The rollout of AI Overviews (AIO) has fundamentally altered the search engine results page (SERP). Recent data indicates that organic CTRs for informational queries featuring AI Overviews dropped from 1.76% to 0.61% between late 2024 and late 2025 impact of AI Overviews on organic CTR.

While this appears destructive to the open web ecosystem, it acts as a defensive moat for Google’s monetization. By keeping users within the Google ecosystem ("zero-click" searches), the company shifts inventory from organic referral traffic to owned-and-operated surfaces where ad injection is controlled exclusively by Google. However, this strategy complicates the regulatory landscape. The U.S. Department of Justice (DOJ) and a coalition of states filed a cross-appeal in February 2026, challenging a prior ruling that stopped short of breaking up the company. The DOJ is explicitly seeking the divestiture of Chrome and a ban on default search agreements with partners like Apple DOJ cross-appeal status. This creates a binary execution risk: if Google loses the distribution dominance provided by Chrome and iOS defaults, its "full stack" AI advantage becomes the primary, and perhaps only, defense against user churn.

| Management Incentives and Cloud Execution |

Management’s compensation structure is heavily weighted toward relative performance, aligning executive incentives with shareholder returns. CEO Sundar Pichai’s equity awards are linked to Alphabet’s Total Shareholder Return (TSR) relative to the S&P 100, with payouts scaling up to 200% for performance above the 75th percentile CEO compensation metrics. This structure incentivizes the protection of the stock multiple through margin preservation and share buybacks, rather than purely experimental moonshots.

This discipline is visible in the Google Cloud segment, which has transitioned from a loss-leader to a profit driver. Cloud revenue grew 32% year-over-year in Q2 2025, reaching $13.6 billion, with operating margins expanding significantly Google Cloud Q2 2025 revenue. The mechanism here is the convergence of AI training demand and cloud infrastructure; as enterprise customers like Citadel adopt Google’s AI Hypercomputer and TPUs, they lock into the ecosystem, increasing switching costs and lifetime value Cloud customer demand.

| Long-Dated Optionality: The "Other Bets" Graduation |

A key differentiator for Alphabet in the "Mag 7" cohort is the commercial maturation of its "Other Bets," which are shifting from R&D cost centers to asset-backed valuation drivers.

Waymo has achieved a critical escape velocity. In February 2026, the autonomous driving unit raised $16 billion in external funding at a valuation of $126 billion Waymo $126B valuation. This valuation establishes a floor for Alphabet’s equity that is uncorrelated with the advertising cycle. The capital is funding aggressive expansion into international markets like London and Tokyo, signaling that the technology has moved from pilot to commercial scaling Waymo international expansion.

Simultaneously, Isomorphic Labs is demonstrating the financial viability of AI in biology. The unit raised $600 million in its first external round, validating its platform for AI-driven drug discovery Isomorphic Labs funding. Furthermore, the Google Quantum AI team achieved a technical breakthrough with the "Willow" chip, demonstrating error correction capabilities that reduce errors exponentially as qubits scale, a milestone essential for commercial fault-tolerant quantum computing Willow quantum chip breakthrough.

| Execution Risks and Tradeoffs |

The primary execution risk remains the Innovator’s Dilemma in Search. By aggressively pushing AI Overviews to compete with Perplexity and OpenAI, Google degrades the economics of its search partners and potentially its own high-margin ad inventory in the short term. The decline in organic and paid click-through rates suggests a friction-heavy transition period where monetization per query may drop before new ad formats (ads within AI responses) fully mature CTR decline data. Additionally, the continued reliance on custom silicon (TPUs) creates a divergence from the Nvidia-centric industry standard; while this offers cost advantages, it requires flawless execution in chip design to prevent a hardware performance gap.

In summary, Alphabet’s strategy is a massive capital-intensive bet on vertical integration, owning the silicon, the data center, the model, and the user interface. While the antitrust overhang is severe, the successful external capitalization of Waymo and Isomorphic Labs provides significant downside protection, creating a sum-of-the-parts valuation floor that many investors may be underappreciating.

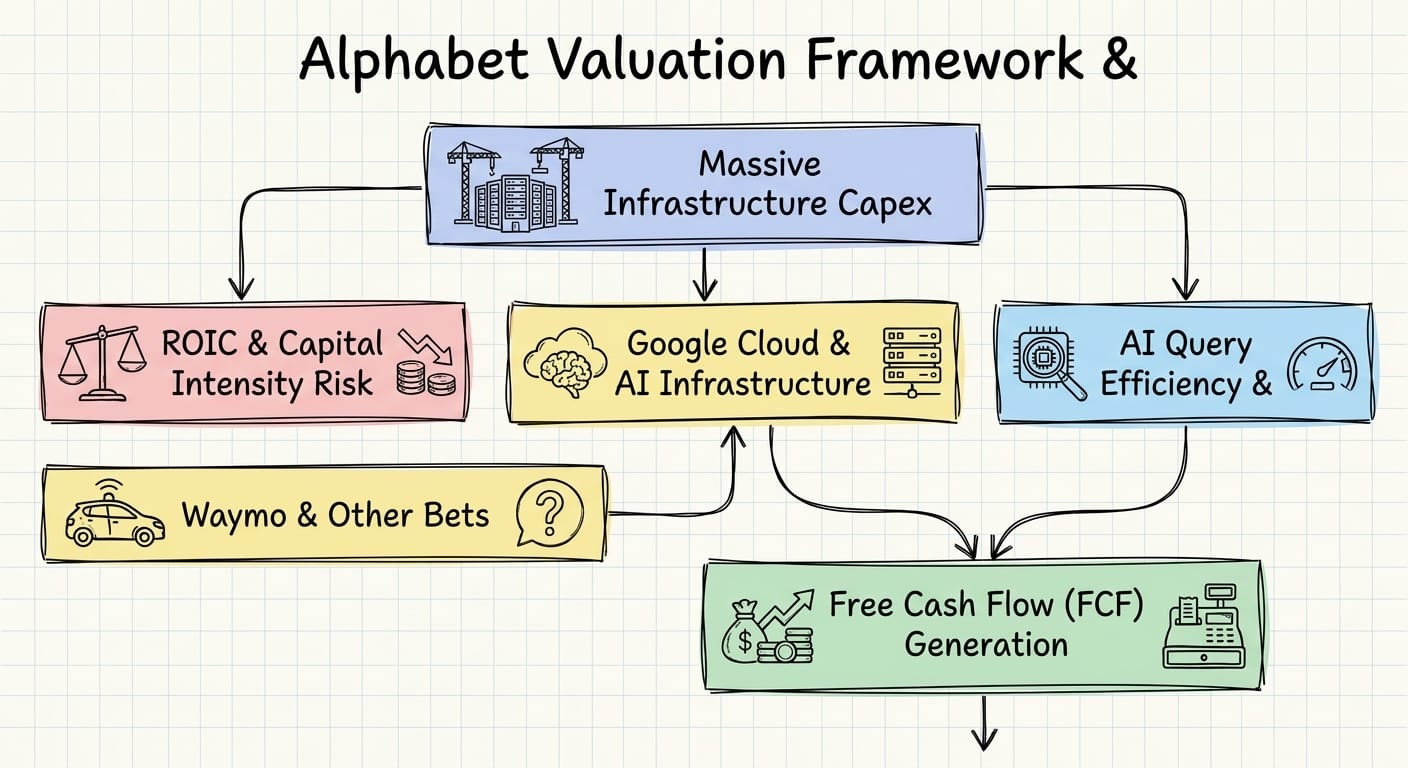

| Valuation Framework & Return Drivers |

To properly assess Alphabet in the current market regime, investors must dismantle the monolithic "Internet proxy" view and value the company as three distinct distinct assets with divergent capital intensity, growth profiles, and return horizons: a mature digital utility (Services), a hyper-scaling infrastructure arm (Cloud), and a validated venture portfolio (Waymo/Other Bets). The market’s obsession with the "AI disruption" narrative for Search often obscures the mechanical reality of Alphabet’s capital allocation and the causal chain between its massive infrastructure spend and future free cash flow (FCF) generation.

| Source: P&L Post |

| The Sum-of-the-Parts (SOTP) Reality |

The most rigorous framework for valuing Alphabet separates the mature cash flows of Google Services from the capital-intensive growth of Google Cloud and the optionality of Other Bets. This approach isolates the specific variables driving returns in each segment, preventing the obscuring of Cloud's margin expansion by Search's capex cycles.

1. Google Services (Search, YouTube, Ads): The Digital Utility This segment generated $87.1 billion in revenue in Q3 2025, growing 14% year-over-year Google Services revenue growth. Valuation here should be driven by a multiple on unlevered free cash flow, adjusted for a "terminal risk" discount related to AI disintermediation. The critical variable is operating margin stability. While the GAAP operating margin was 30.5% in Q3 2025, the figure excluding the European Commission fine stood at 33.9%, demonstrating underlying resilience despite the AI platform shift adjusted operating margin.

Consensus frequently misprices the impact of AI on Search margins by extrapolating early, inefficient compute costs. Google has achieved a 33-fold reduction in energy cost per AI query over the last year AI query energy reduction. This efficiency gain suggests that the "margin collapse" thesis is structurally flawed; the primary driver of Services valuation remains ad load preservation within AI Overviews, not pure inference costs.

2. Google Cloud Platform (GCP): The Hyper-Growth Engine GCP is often undervalued when blended with Search. In Q3 2025, Cloud revenue accelerated to $15.2 billion (+34% YoY), outpacing the broader business Cloud revenue acceleration. More importantly, the backlog, contracted revenue not yet recognized, surged to $155 billion, an 82% year-over-year increase Cloud backlog growth.

This backlog creates high visibility for future cash flows, justifying a higher multiple closer to pure-play SaaS or infrastructure peers. The causal mechanism here is the conversion of AI training demand into long-term inference contracts. As customers like Anthropic and enterprise clients commit to multi-year compute deals, Cloud revenue becomes recurring and sticky, warranting a valuation premium that blunts the cyclicality of the ad market.

3. Other Bets: Validated Optionality (Waymo) For years, Other Bets was treated as a negative value, a "tax" on earnings. That framework is now obsolete. Waymo raised $16 billion in an external funding round at a $126 billion post-money valuation in early 2026 Waymo valuation. With over 400,000 paid weekly rides and 15 million rides delivered in 2025 alone Waymo ride volume, Waymo has transitioned from a R&D expense to a commercial asset with a market-validated price tag. A correct valuation framework must now add ~$120B+ to Alphabet’s enterprise value rather than deducting its operating losses.

| The Capex Cycle and ROIC Implications |

The single biggest variable determining long-term shareholder returns is the efficiency of Alphabet’s capital expenditures. The company guided 2025 capex to a range of $91 billion to $93 billion 2025 capex guidance. This massive outlay effectively suppresses free cash flow in the short term, creating a "valley" in FCF yield.

Investors must assess whether this is a "land grab" with poor returns or a necessary wide-moat construction. The mechanic to watch is the Capex-to-Revenue lag. The $155 billion cloud backlog suggests that today’s infrastructure spend is successfully capturing future revenue. If Alphabet were spending $93 billion without a corresponding spike in backlog, it would signal capital destruction. Instead, the data indicates that the capex is demand-pull, not supply-push.

However, the risk to ROIC (Return on Invested Capital) is real. If AI hardware depreciates faster than the typical 3-5 year server cycle due to rapid obsolescence of GPU generations, the depreciation expense will permanently structurally lower GAAP earnings. Valuation models must account for a "capital intensity penalty," lowering the target P/E multiple for the aggregate business to reflect that each dollar of revenue now requires more tangible assets to generate than in the pre-AI era.

| Sensitivity Analysis and Scenarios |

- Bear Case (Value Trap): AI commoditizes information retrieval, forcing Google to increase traffic acquisition costs (TAC) to defend share. Cloud growth slows as AI training demand plateaus, leaving the company with overbuilt capacity. Waymo fails to scale beyond its current six metro areas due to regulatory caps.

- Result: Multiple compression to 12-14x earnings; returns driven solely by buybacks.

- Base Case (Durability): Search volumes grow low-single digits while ad pricing holds. Cloud margins expand toward 30% (approaching AWS levels) as the business scales. Capex stabilizes as a percentage of revenue in 2027.

- Result: Low double-digit annual returns composed of earnings growth + ~3% buyback yield.

- Bull Case (AI Dividend): AI Overviews increase query volume and conversion rates, allowing Alphabet to monetize higher-value commercial intent. Cloud maintains >30% growth for 3+ years driven by inference workloads. Waymo successfully launches in international markets like Tokyo and London Waymo international expansion.

- Result: Multiple expansion re-rating to 20-22x; Waymo spin-off unlocks massive value.

| Capital Returns as Downside Protection |

Finally, the floor for the valuation is set by capital returns. Alphabet’s massive cash pile allows it to aggressively repurchase shares, serving as an automatic stabilizer for EPS. With a $70 billion buyback authorization active share buyback authorization, the company effectively creates a put option on its own stock. If the market irrationally discounts the AI risk, the company’s own bid provides mechanical support to the share price, enhancing the long-term IRR for remaining shareholders.

| What the Market Is Mispricing |

The consensus view on Alphabet currently reflects a profound dissonance between the company’s structural durability and its valuation. While the broader "Magnificent Seven" cohort trades at premium multiples reflecting indefinite AI-driven growth, Alphabet trades at a discount that implies imminent terminal decline or structural displacement. The market has anchored its thesis on three primary fears: the cannibalization of Search revenue by generative AI, the erosion of margins due to soaring compute costs, and the existential threat of regulatory breakup.

| GOOGL trades significantly below its estimated fair value based on this visual model. (Yahoo Finance) |

However, a mechanism-driven analysis reveals that the market is mispricing Alphabet’s vertical integration, specifically its ability to control the unit economics of the AI transition better than any competitor. The current valuation effectively prices in a "worst-case" scenario for Search disruption while assigning zero or negative value to optionality in autonomous transport and the structural shift of television viewership to YouTube. The mispricing exists because investors are linearizing the costs of AI infrastructure (the "Nvidia Tax") without accounting for Alphabet’s proprietary silicon advantage, which creates a distinct cost-curve arbitrage unavailable to Microsoft, Meta, or OpenAI.

| The Inference Cost Arbitrage |

The most significant analytical error in the consensus bear case is the assumption that Alphabet faces the same margin compression as its peers as AI workloads shift from training to inference. The market assumes that serving AI-generated answers will permanently depress operating margins due to the high capital intensity of GPU procurement. This ignores Alphabet’s decade-long head start in custom silicon. While competitors must pay gross margin premiums to Nvidia for H100s and Blackwell chips, Alphabet offloads the bulk of its internal inference volume to Tensor Processing Units (TPUs).

Data indicates that specialized ASICs like TPUs are creating a bifurcated cost structure in the AI industry. For high-volume inference workloads, Google’s custom infrastructure delivers significantly better cost-performance ratios than general-purpose GPUs. Companies migrating specifically to TPUs for inference have reported substantial reductions in monthly operational spend, with some high-profile cases seeing costs drop by approximately 65% after switching from Nvidia-based infrastructure inference cost reduction. This is not merely a technical detail; it is a financial firewall. As inference demand scales to projected levels, potentially consuming 75% of all AI compute resources by 2030, Alphabet’s ability to serve tokens at a lower marginal cost than competitors relying on merchant silicon constitutes a structural gross margin advantage inference market share projections. The market is pricing Alphabet’s CAPEX as a drag on free cash flow, rather than recognizing it as an investment in a lower-cost operating model that competitors cannot easily replicate.

| The Search Cannibalization Fallacy |

Investors have priced Alphabet under the assumption that Generative AI is deflationary for the core Search business, that users will search less, and that "zero-click" answers will destroy ad inventory. This narrative ignores the elasticity of demand for information and the proven adaptability of the ad stack. Recent disclosures confirm that AI-infused search experiences are not cannibalizing monetization; rather, AI Overviews are effectively monetizing at parity with traditional search results monetization parity.

Furthermore, the integration of AI is driving an acceleration in query volume rather than a substitution effect. Search revenue growth accelerated to the mid-teens in late 2025, driven by higher engagement with AI-augmented features Search revenue acceleration. The introduction of ads directly within AI-generated summaries opens new inventory that did not previously exist, converting informational queries into commercial opportunities closer to the point of intent ads in AI Overviews. The market misprices this transition as a zero-sum game between "links" and "answers," failing to recognize that improved answer quality historically correlates with increased query frequency and higher commercial intent. The structural risk is not that Google loses search volume, but that the market fails to model the incremental revenue from AI-driven query expansion.

| The Hidden Value of Waymo |

Perhaps the most glaring omission in the current valuation is the treatment of Waymo. For years, investors have treated Waymo as a "moonshot" cost center, effectively assigning it a negative value in Sum-of-the-Parts (SOTP) analyses due to its operating losses. This view is now obsolete. Waymo has transitioned from R&D experimentation to commercial scaling with unit economics that are proving the viability of the robotaxi business model.

Recent funding rounds have re-rated the division significantly, with valuations surging from roughly $45 billion to approximately $126 billion following capital injections from sophisticated external investors Waymo valuation increase. The service has tripled its paid ride volume year-over-year, operating fully driverless fleets in major metropolitan areas like San Francisco, Phoenix, and Los Angeles Waymo ride volume growth. By pricing Alphabet as a pure-play advertising business facing secular headwinds, the market is offering the world's leader in autonomous driving, a potential trillion-dollar TAM, effectively for free. A spin-off or continued external capitalization of Waymo provides a hard catalyst to unlock this value, serving as a powerful hedge against core advertising volatility.

| The Regulatory Discount & YouTube's Moat |

Finally, the antitrust discount applied to Alphabet is overstated relative to the realistic timeline of judicial outcomes. While the Department of Justice has proposed severe remedies, including the divestiture of Chrome, the legal appeals process is expected to extend well into 2026 and beyond, creating a status quo that preserves Alphabet's cash generation for years antitrust appeals timeline. The market prices the headline risk of a breakup immediately, ignoring the time value of continued monopoly rents and the high probability of watered-down final remedies.

Simultaneously, the market underappreciates the defensive moat of YouTube. It is no longer just a social video platform but the dominant player in Connected TV (CTV) viewership. YouTube has surpassed Netflix in U.S. TV screen time, cementing itself as the default operating system for the living room YouTube vs Netflix TV share. This shift from mobile to living room viewing opens up "TV-like" ad budgets that are stickier and higher-margin than mobile web inventory. The consensus treats YouTube as mature, missing the inflection point where it begins to capture linear TV ad dollars at scale due to its dominance in streaming watch time YouTube living room dominance.

In conclusion, the mispricing exists because the market is focused on the threat of AI disruption without calculating the mitigation provided by proprietary silicon, and the upside of new vertical integrations. Alphabet is priced for a disruption that its infrastructure advantage allows it to weather better than any peer.

| Key Metrics & Signals to Monitor |

The transition from a stable, utility-like search monopoly to an aggressive, capital-intensive AI conglomerate requires a fundamental recalibration of how investors evaluate Alphabet. For nearly a decade, the primary algorithm for valuing GOOGL was a simple function of paid click growth and cost-per-click (CPC) stability, adjusted for Traffic Acquisition Costs (TAC). That model is now insufficient. The company is currently navigating a period of maximum capital intensity to secure a new computing platform, necessitating a shift in focus toward metrics that quantify the efficiency of this spend and the durability of the legacy moat.

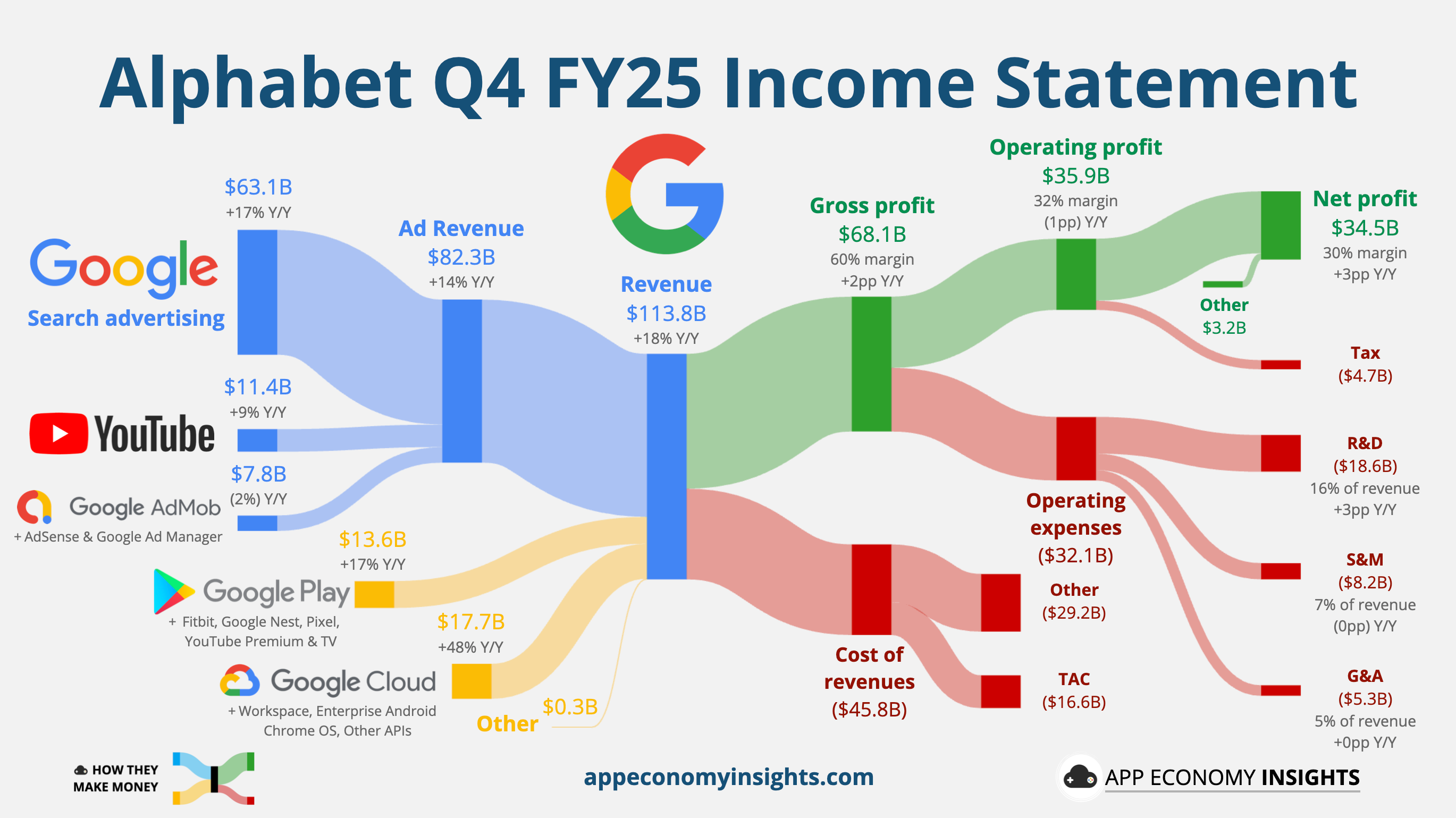

| Google Cloud revenue experienced significant growth in Q4 FY25, reaching $17.7 billion and increasing 48% year-over-year. (App Economy Insights) |

To validate the thesis that Alphabet can successfully bridge the gap between the mobile internet era and the AI agent era, investors must look beyond headline earnings per share (EPS) and scrutinize four specific mechanism-driven signals. These metrics isolate structural performance from cyclical noise and provide the clearest indication of whether the company is compounding value or merely setting fire to cash in a defensive panic.

| 1. The AI Return on Invested Capital (ROIC) Proxy |

The most immediate risk to shareholder value is not a loss of search share, but an undisciplined capital cycle. Alphabet has committed to a historic infrastructure buildout, with full-year 2025 capital expenditures guided to a massive range. The company projected spending levels between $91 billion and $93 billion 2025 capex outlook, a figure that exceeds the total annual revenue of most S&P 500 companies. While management describes this as a "land grab" necessary for future capacity, the sheer scale raises the bar for required returns.

The critical signal here is the ratio of incremental Cloud revenue to incremental Capex. While imperfect, this proxy helps determine if the infrastructure is being monetized or merely accumulated. In the third quarter of 2025, Google Cloud revenue accelerated significantly, growing 34% year-over-year cloud revenue growth. If this revenue acceleration persists while capex stabilizes or grows at a slower rate in 2026, it confirms that the "training phase" is transitioning to the "inference/commercialization phase," where margins naturally expand. Conversely, if capex continues to grow at 60-80% year-over-year while Cloud revenue growth plateaus in the 30% range, it suggests that the unit economics of AI are deteriorating due to pricing pressure or hardware obsolescence.

| 2. Cloud Backlog Conversion Velocity |

While revenue describes the past, the backlog describes the future. The most bullish signal in recent disclosures is not the top-line growth, but the explosion in committed remaining performance obligations (cRPO). The company reported a staggering backlog of $155 billion cloud backlog ending Q3 2025, representing a 46% sequential increase from the previous quarter sequential backlog growth.

This metric is the "check engine" light for enterprise AI adoption. A swelling backlog confirms that large enterprises are not just piloting Gemini models but signing multi-year, high-value commitments that lock them into the Google ecosystem. Investors must monitor the conversion velocity, the rate at which this backlog recognizes into revenue. A rapidly growing backlog with lagging revenue recognition could indicate deployment bottlenecks (e.g., customers signing deals but unable to productionize AI workflows), whereas a synchronized rise suggests healthy execution. Furthermore, the mix of this backlog matters; the surge is partly driven by an increase in deals valued over $1 billion billion-dollar deal volume, signaling that Google is finally displacing legacy incumbents in core IT infrastructure rather than just winning peripheral workloads.

| 3. Search Share Floor vs. Query Volume Expansion |

The consensus bear case relies on the idea that Generative AI answers (via ChatGPT or Perplexity) are a direct substitute for Google Search. If this were true, Google’s market share would be collapsing. Instead, the data suggests a slow erosion rather than a cliff edge, with global share dipping slightly below 90% in late 2024 market share decline. However, share percentage is a vanity metric if the total volume of queries is expanding.

The metric to watch is absolute query volume growth combined with commercial query density. If users are shifting "informational" queries (e.g., "how to tie a tie") to chatbots but retaining "commercial" queries (e.g., "buy nike running shoes") on Google, Alphabet’s monetization engine remains intact. In fact, fewer low-value queries could theoretically improve margins by reducing processing costs. The rollout of AI Overviews to over a billion users is the key test here. Investors should monitor whether the introduction of these AI summaries leads to a "zero-click" environment that starves the ad ecosystem, or if it increases total session time. Early data suggests the Gemini app has reached significant scale with 650 million monthly active users Gemini app users, serving as a defensive flank that keeps users inside the Google data loop even if they bypass traditional search. A stabilization of market share around 88-89% combined with double-digit growth in "Search & Other" revenue would falsify the disruption thesis.

| 4. The "Other Bets" Graduation: Waymo’s Unit Economics |

For years, "Other Bets" was a euphemism for shareholder capital destruction. This narrative flipped in late 2025. Waymo is no longer a science project; it is a revenue-generating commercial transport network. With weekly trips surpassing 150,000 to 250,000 weekly trip volume and annualized revenue run rates approaching $1 billion, Waymo is entering the "Uber phase" of scaling.

The signal to monitor is not just top-line growth, but the reduction in operating losses relative to mileage. The division reported a loss of $1.4 billion on $344 million in revenue Waymo financial performance for Q3 2025. While deep in the red, the trajectory of this loss is critical. If revenue doubles in 2026 while losses remain flat, it proves operating leverage exists in the robotaxi model (hardware costs and teleoperation ratios are improving). This would transform Waymo from a valuation drag into a high-growth asset potentially worth $100 billion+ as a spin-off candidate, providing a massive "call option" that protects the stock’s downside.

| 5. Regulatory TAC Dynamics |

Finally, the Department of Justice’s antitrust victory regarding search distribution creates a binary risk focused on Traffic Acquisition Costs (TAC). The courts have ruled Google’s exclusive default agreements illegal, and the DOJ has filed notices to cross-appeal for stricter remedies DOJ cross-appeal.

The metric to watch is the TAC rate as a percentage of Search revenue. Paradoxically, losing the ability to pay Apple $20 billion annually for default status could increase Alphabet’s immediate free cash flow, provided users switch back to Google voluntarily (the "muscle memory" thesis). If the TAC rate drops significantly in 2026 without a corresponding drop in mobile search volume, the antitrust ruling effectively acts as a government-mandated cost-cutting program. However, if volume bleeds to Bing or Siri-native search, the thesis breaks. Investors must parse the quarterly "Google Services" operating margin; a spike in margin accompanied by flat revenue would confirm that the distribution payments were largely redundant, proving the structural durability of the brand.

| Risks to the Thesis |

The bear case for Alphabet is no longer a theoretical exercise in valuation compression; it is a structural dismantling of the mechanisms that generated the most lucrative cash flow stream in corporate history. While the market fixates on the race for generative AI supremacy, the graver threat lies in the simultaneous erosion of Google’s distribution monopoly and the forced re-architecture of its unit economics. The thesis for long-term durability rests on the assumption that Alphabet can transition from a utility-grade distributor of links to an AI-first answer engine without destroying its margins or losing its distribution dominance. This transition faces three compounding failure modes: regulatory de-moating, margin dilution through compute intensity, and cultural inertia accelerating talent flight.

| This conceptual illustration uses a board game analogy to represent Google's position in the search market. (AdExchanger) |

| Structural Decay of the Distribution Monopoly |

The primary structural risk is not the existence of better search technology, but the legal dismantling of the distribution rails that ensure Google Search remains the default habit for billions of users. The U.S. Department of Justice’s victory in the search antitrust trial has moved beyond liability to remedies that fundamentally alter the competitive landscape. Federal Judge Amit Mehta’s ruling in August 2024 established that Google illegally maintained its monopoly, and the subsequent remedies phase has targeted the exclusionary contracts that serve as the company's defensive moat.

The court rejected the most draconian structural remedy, a forced divestiture of Chrome, but imposed behavioral restrictions that may prove more damaging to long-term stickiness. The ruling prohibits Google from conditioning revenue share on exclusive default status and mandates that the company’s massive search agreements, including the estimated $20 billion annual payment to Apple, be subject to annual rebidding rather than multi-year lock-ins annual rebidding of default contracts. This introduces perpetual uncertainty into Google’s traffic acquisition costs (TAC) and gives competitors like Microsoft or emerging AI players a yearly window to outbid or displace Google on Safari and Android devices. Furthermore, the 12-month limit on default agreements prevents Google from securing long-term distribution stability, forcing it to compete on merit and price continuously 12-month default limit.

Simultaneously, the Ad Tech antitrust case presents a parallel threat to the company's display advertising machinery. Following a ruling in April 2025 that Google monopolized the publisher ad server and ad exchange markets, the Department of Justice is pursuing the divestiture of Google Ad Manager (DFP and AdX) illegal monopoly in advertising business. Unlike the search remedies, which are behavioral, a forced breakup of the ad tech stack would sever the data feedback loop that allows Google to dominate the open web's monetization, reducing its ability to leverage data across its ecosystem.

| The AI Margin Compression Trap |

Even if Google retains its market share, the transition to Generative AI creates a mechanical pressure on profitability that cannot be fully offset by efficiency gains. The core economic risk is the shift from a high-margin "retrieve and rank" model to a lower-margin "compute and generate" model. While management has signaled that AI Overviews are monetizing at parity with traditional search monetization parity claims, this assertion relies on A/B testing within a controlled environment and may not account for the long-term shift in user intent from clicking ads to consuming zero-click answers.

The cost structure of this transition is capital intensive. Alphabet has guided for 2025 capital expenditures to reach $91 billion to $93 billion, a massive step-up driven primarily by the need for AI infrastructure 2025 capital expenditures forecast. This spending creates a significant depreciation drag on earnings before the revenue uplift from AI services is fully realized. Third-party analysis suggests that while energy costs per query are dropping, the net cost of an AI-powered search remains multiples higher than a traditional query, creating a structural headwind to operating margins energy cost of AI queries.

Furthermore, the introduction of AI Overviews effectively reduces the real estate available for organic links, forcing advertisers to bid more aggressively for scarcer inventory. While this may temporarily boost ad revenue through cost-per-click (CPC) inflation, reported to be up 18–25% in retail sectors, it risks alienating the small business ecosystem that cannot sustain higher customer acquisition costs CPC inflation in retail. If advertisers shift budget to platforms with better ROI or lower friction, Google’s pricing power could erode just as its capital intensity peaks.

| Cultural Inertia and Talent Hemorrhage |

Beyond regulation and economics, Alphabet faces an execution risk rooted in its corporate culture. The "Peacetime Google" that prioritized academic research and consensus decision-making has struggled to adapt to the "Wartime" urgency required by the AI arms race. This cultural friction was vividly illustrated by the Gemini image generation controversy, where the model refused to generate historically accurate images due to over-tuned diversity guardrails, forcing a humiliating pause of the feature Gemini image generation suspension. This failure was not merely a technical glitch but a symptom of a bureaucratic alignment process that prioritized safety and optical neutrality over product utility and accuracy.

This environment has catalyzed a talent drain of top-tier researchers to more agile competitors. Key personnel from Google DeepMind and the core AI teams have departed for OpenAI, Anthropic, and Meta, lured by more aggressive shipping schedules and lucrative compensation packages researcher departures to rivals. The loss of foundational talent like the co-creators of key transformer models weakens Alphabet's intellectual property moat. If the engineers capable of building the next generation of models believe they can execute faster at Anthropic or Meta, Google’s massive compute advantage becomes a depreciating asset managed by B-tier talent.

| Downside Scenarios and Thesis Failure |

The thesis breaks if the convergence of these risks creates a negative flywheel:

- 1. Distribution Collapse: Regulatory remedies end the Apple default deal, causing Google to lose 10-15% of high-value iOS query volume to a competitor who wins the annual bid.

- 2. Margin Reset: To retain the remaining users, Google is forced to deploy expensive AI models for all queries, compressing operating margins to the low 20% range permanently.

- 3. Ad Flight: Advertisers, squeezed by AI-driven CPC inflation and seeing lower conversion rates from "zero-click" searches, diversify spend to Amazon and TikTok.

- 4. Valuation De-rating: The market re-rates Alphabet not as a growth compounder, but as a regulated utility with declining returns on invested capital, permanently impairing the multiple.

Investors must weigh the probability that the "moat" was never the technology, but simply the distribution contracts that are now legally void.

| Alphabet’s AI pivot strengthens its infrastructure edge |

Alphabet remains the preeminent global utility for information, but its investment thesis has fundamentally evolved. The company is no longer just a media aggregator monetizing attention through simple auctions. Instead, it has become a vertically integrated infrastructure powerhouse. The transition from distributing links to providing synthesized intelligence requires massive capital, yet Alphabet is uniquely positioned to fund this shift. Its primary drivers are the enduring cash flows from Search and YouTube, which provide the liquidity needed for a generational investment in proprietary silicon. By leveraging its Tensor Processing Units, the company can provide AI-driven answers at a lower unit cost than competitors who rely on third-party hardware. This structural advantage, combined with the rapid scaling of Google Cloud and the emerging commercial viability of Waymo, suggests that the market is overestimating the threat of terminal decline.

However, the path forward is not without significant structural risks. The most pressing threat is the regulatory dismantling of the distribution rails that have historically protected the Search engine. Legal challenges to exclusionary contracts could force a fundamental re-architecture of how Google reaches users, potentially eroding its volume-driven pricing power. Furthermore, the transition to compute-intensive synthesis carries the risk of margin dilution if the efficiency gains from internal projects do not materialize. If the cost to serve an AI-generated answer remains significantly higher than the cost of a traditional query, the company's historically high operating margins could face permanent compression. Cultural inertia also remains a factor, as the company must pivot its talent and execution toward a new competitive reality.

The current outlook on Alphabet would change if there were clear signs of a structural breakdown in its economic engine. Specifically, a sustained loss in query volume to independent AI agents or a failure to maintain the cost advantage of its internal silicon would invalidate the thesis. Additionally, if regulatory remedies mandate a forced divestiture of core assets like Chrome or Android, the integrated data flywheel would be broken. Until such shifts occur, Alphabet’s combination of high-fidelity user intent and superior infrastructure economics makes it a resilient leader in the new era of generative intelligence.