Mortgage rates finally blinked lower after a five-week climb, but the relief looks brittle. Freddie Mac’s 30-year average slipped to 6.37 percent from 6.46 percent a week earlier as the U.S.-Iran ceasefire cooled some of the panic around oil prices and inflation. The bigger question is whether that turns into a real spring thaw for housing, or just a pause before the next inflation print and another turn higher in yields.

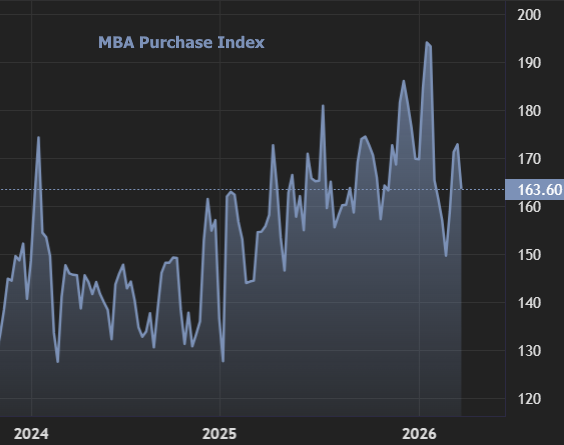

The market is still carrying the damage from the war. Mortgage applications, new listings and pending sales have all slowed, and the Mortgage Bankers Association said the unadjusted purchase index for the week ending April 3 was 7 percent below the same week a year ago, the first year-over-year decline since January 2025. That is the kind of stall that keeps sellers cautious and leaves buyers staring at listings rather than making offers.

There is still some appetite under the surface. Zillow said average daily page views of for-sale listings were up 32 percent from a year earlier, while applications for lower-rate products such as adjustable-rate mortgages and FHA loans have picked up. Even so, economists quoted in the reports said the market remains in a “holding pattern,” with inflation expected to stay sticky if energy and shipping costs keep pressure on the economy. Affordability and supply are pushing first-time buyers later in life too, and the National Association of Realtors said the typical age of first-time buyers has climbed to 40.

The mix leaves housing in an awkward spot: lower borrowing costs would help demand, but cheaper money could also pull more buyers into a market where inventory is already fragile. If rates keep falling, buyers may get a better shot at financing, but not necessarily more homes to choose from. If rates rise again, the slowdown can deepen fast.