Mortgage rates finally broke their five-week climb, with Freddie Mac putting the average 30-year fixed loan at 6.37 percent, down from 6.46 percent a week earlier. The relief is real, but it is fragile: the drop came after a U.S.-Iran ceasefire cooled fears that oil prices and inflation would keep pushing borrowing costs higher, and the latest move still leaves rates well above February’s lows.

The mechanics are familiar and brutal. Mortgage pricing tends to shadow the 10-year Treasury yield, which eased alongside the ceasefire, while lenders also watched energy and inflation signals. Yahoo Finance noted the same pattern, warning that March inflation data due April 10 could keep the recent dip from lasting if prices stay sticky. In other words, buyers got a brief opening, not a clean break.

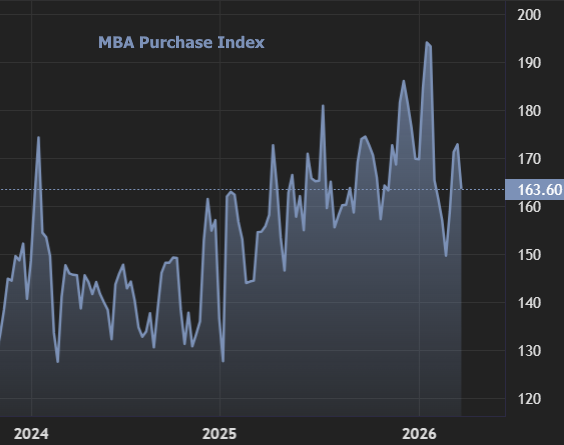

The housing market is already feeling the strain. The Mortgage Bankers Association said the unadjusted purchase index for the week ending April 3 was 7 percent below the same week a year ago, the first year-over-year decline since January 2025. Redfin reported new listings were down 2.6 percent from a year earlier, while Zillow said page views for for-sale listings jumped 32 percent, a sign that would-be buyers are still prowling even as they hesitate to commit. Sellers are getting the message too, and that can keep inventory tight if demand stays weak.

Longer term, the squeeze is reshaping who gets in and when. The age of first-time buyers has climbed to 40, according to the National Association of Realtors, as affordability and supply both bite. For families trying to buy now, lower rates and more homes may not arrive together, and the market’s current pause could end up pushing more people to wait longer, borrow differently, or give up on the traditional starter-home route altogether.