The spring housing season was setting up for a long-awaited thaw, then mortgage rates slammed back into the mid-sixes. Freddie Mac’s average 30-year fixed rate rose to 6.38 percent for a fourth straight week, a move that puts affordability back in the driver’s seat just as more listings are finally showing up.

The mechanics are simple and unforgiving: mortgage rates tend to follow the 10-year Treasury yield, and CNN notes yields have climbed as markets price in inflation risk tied to the Iran conflict. That rate jump is not academic. On a $450,000 home with 20 percent down, CNN calculates a buyer locking today instead of a month ago pays about $1,120 more per year. A spring shopper who thought sub-6 percent mortgages were back is suddenly staring at a monthly payment that can blow up a budget, or a preapproval.

Here’s the tension: the market is getting more buyer-friendly, but financing is re-tightening. Realtor.com’s weekly data shows inventory up 7.8 percent year to date and a median list price down 1.9 percent from a year earlier, the 22nd straight week of flat-to-negative annual price growth. Yet rates are moving the other way, and Realtor.com also flags that the pace of inventory recovery has slowed, with new listings still running below last year’s year-to-date pace.

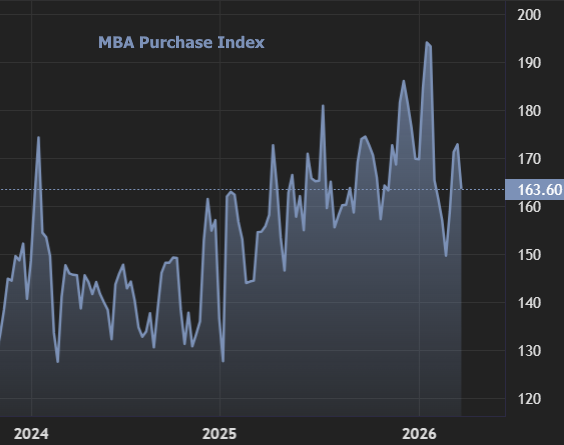

For buyers and sellers, the near-term playbook looks like this: demand cools first, then negotiation power shifts. CNN points to mortgage applications falling 10.5 percent and Redfin data showing contract cancellations hitting a February record share, classic signs that shoppers are hesitating, repricing, or walking. Yahoo Finance’s rate sheet puts numbers on the squeeze, with Zillow data showing 15-year mortgages around 5.85 percent and adjustable-rate mortgages not offering much relief. If rates stay elevated, sellers may have to meet buyers on price, concessions, or both; if rates retreat again, the extra inventory could convert into actual closings instead of just more open houses.