The spring housing market finally had a pulse, then geopolitics took the air out. The average 30-year fixed mortgage rate jumped to 6.38 percent for a fourth straight week, a sharp reversal from late February when rates briefly dipped below 6 percent and buyers started circling. Now the problem is not a lack of homes, it is a higher cost of money landing right as peak touring season ramps.

The mechanics are simple and brutal: mortgages tend to follow the 10-year Treasury yield, and bond markets have been repricing inflation risk as the Iran conflict rattles energy and broader markets. CNN notes the 10-year yield hit levels not seen since July, pushing lenders to raise rates quickly. Realtor.com pins the same 6.38 percent print to Freddie Mac and adds that the move has arrived alongside lower list prices and rising inventory, an odd mix that gives buyers more leverage but makes monthly payments harder to swallow.

- Affordability hit: on a $450,000 home with 20 percent down, locking today versus a month ago costs about $1,120 more per year in payments, according to CNN’s example.

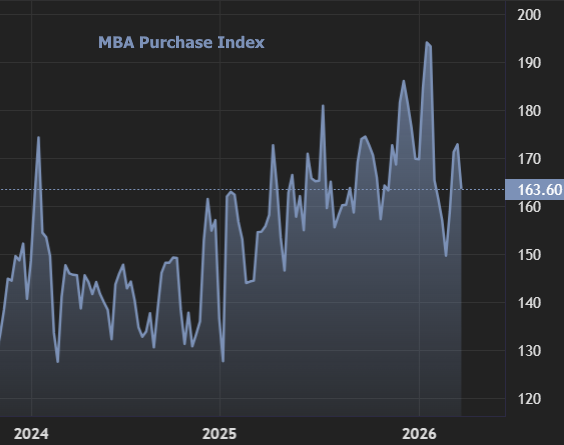

- Demand is flinching: the Mortgage Bankers Association reported mortgage applications fell 10.5 percent last week.

- Supply is improving, but not exploding: Realtor.com says inventory is up 7.8 percent year to date, while new listings are still down year to date versus 2025.

That leaves the market in a buyer-friendlier posture without the clean “rates are falling” catalyst that typically turns more lookers into closers. Yahoo Finance flags that even 15-year loans are nearing 6 percent, which narrows the appeal of trading up to a shorter term, and it reinforces a bigger freeze: homeowners with older, cheaper mortgages have less reason to move. Realtor.com’s data also shows prices drifting lower year over year and homes sitting longer, but the next few weeks hinge on whether rates stabilize, or keep leapfrogging higher and force sellers to cut further to meet buyer math.