A map from MarineTraffic tracks vessel movements through the Strait of Hormuz. Data visualizes global shipping activity near critical Iranian energy infrastructure.

Source: YouTube

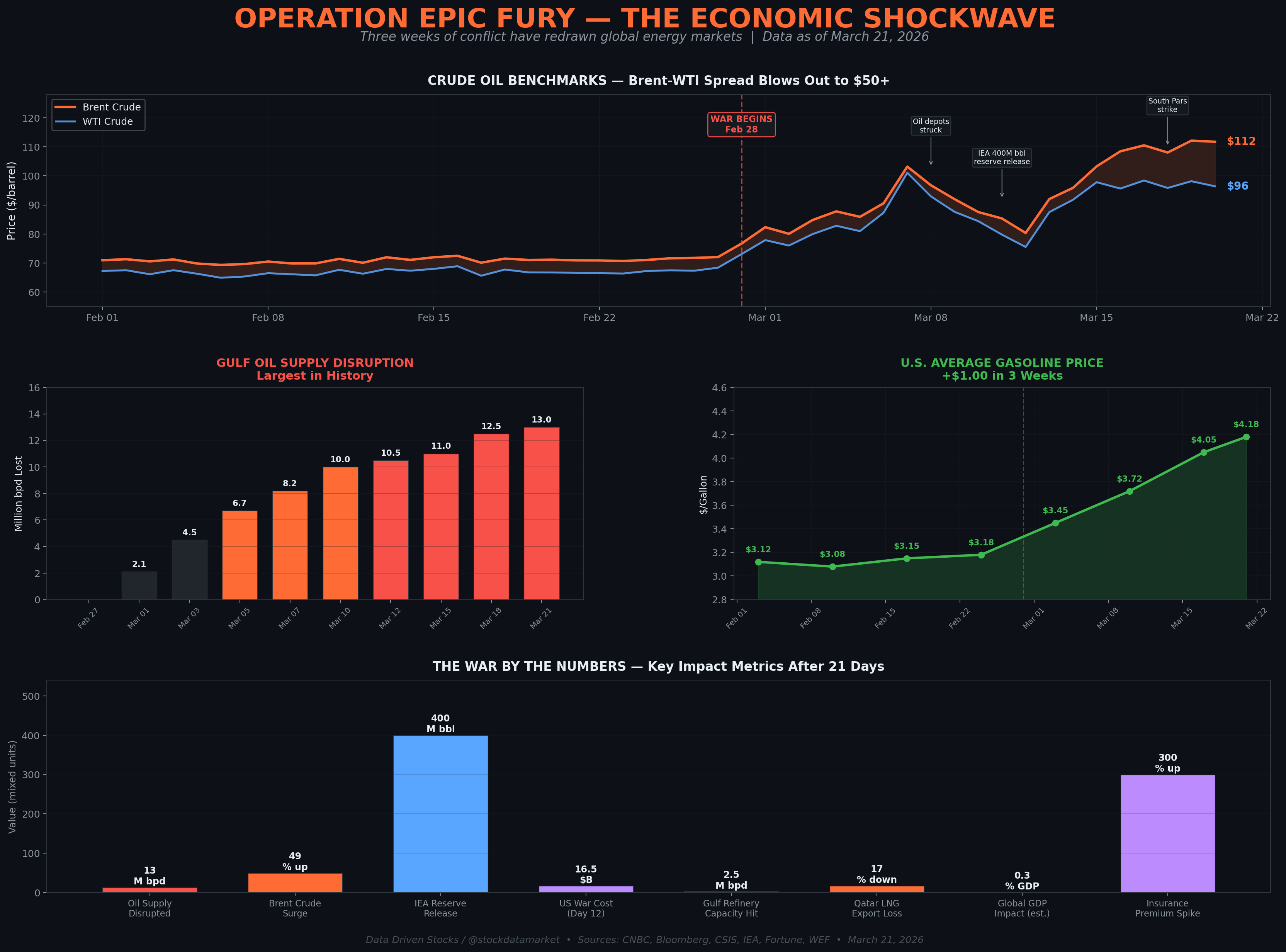

Markets opened the week trading the war, not the data. After President Donald Trump gave Iran 48 hours to reopen the Strait of Hormuz or face strikes on power plants, investors dumped Asian equities, with Japan’s Nikkei and South Korea’s Kospi each falling more than 5 percent, while Europe braced for a similar hit at the open, with the DAX, CAC 40 and FTSE all called lower. The immediate fear is no longer just expensive oil. It is the risk that attacks spread from military targets to civilian energy and water systems across the Gulf, turning a supply shock into a broader economic one.

That risk is already showing up across assets. Reuters reported the dollar firmed as investors sought havens, while 10-year Treasury yields hovered near an eight-month high as traders re-priced inflation and scaled back hopes for Federal Reserve cuts. Oil was volatile rather than straight up, with Brent near $112 a barrel in early trade, but the bigger market problem is duration: if the Strait stays constrained and Gulf infrastructure becomes a target, importers in Europe and Asia face a harsher energy bill just as central banks were trying to keep inflation contained.

There is also a notable split in the market signal. Equity traders are acting as if growth takes the first hit, while currency and rates markets are treating the conflict as an inflationary shock that could keep policy tighter for longer. Reuters noted that before the war, investors had expected two Fed cuts this year, but now one cut looks like a distant prospect. That leaves rate-sensitive corners of the market with little shelter: higher oil squeezes margins and consumers, while higher yields make lofty valuations harder to defend.

For now, traders are watching a deadline with unusually heavy consequences. CNBC reported that Iran has threatened retaliation against regional energy infrastructure and desalination facilities, and Fortune described the scenario as potentially catastrophic if the conflict moves deeper into civilian systems. If neither side backs down, Monday’s selloff could look less like a panic open and more like the market beginning to price a longer war, stickier inflation, and a much narrower path to a soft landing.