U.S. consumers are feeling the shock of the Iran war before the broader economy does. The University of Michigan’s consumer sentiment index fell to 49.8 in April, a record low, even as the ceasefire with Iran took some of the edge off fears about gas prices. Households are still fixated on what the conflict is doing to fuel, food and freight costs, and that is pushing inflation expectations higher just as the stock market keeps setting highs.

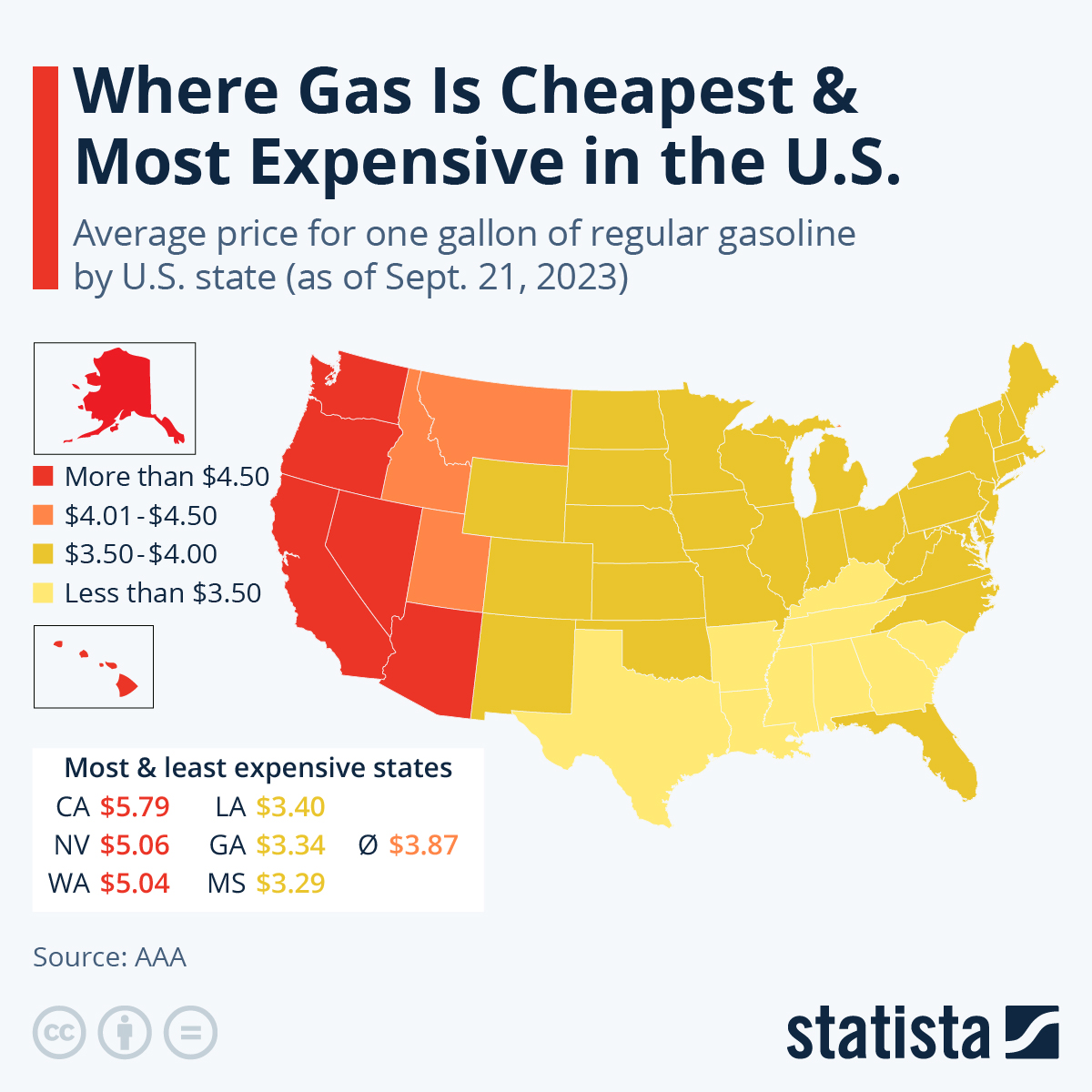

The survey showed one-year inflation expectations jumping to 4.7 percent from 3.8 percent in March, while five-year expectations climbed to 3.5 percent. Joanne Hsu, the survey’s director, said military and diplomatic developments do little for consumers unless they ease supply constraints or lower energy prices. That leaves the price transmission mechanism, from oil to gasoline to diesel to transported goods, front and center. AAA data cited by Yahoo Finance showed gas prices have risen by more than a dollar on average since the war began.

Business surveys are pointing in the same direction, though with a different twist. S&P Global’s flash PMI showed U.S. private-sector activity improving in April, but the recovery was driven largely by stock building in manufacturing as firms rushed to secure supplies before more disruptions hit. Delivery times lengthened to the worst since August 2022, output-price inflation hit a near four-year high, and companies reported higher input costs across energy and commodities. In plain English, companies are moving faster not because demand is roaring, but because they are trying not to get caught short.

That mix leaves policymakers and investors with an uncomfortable tradeoff. The economy is not rolling over, but it is also not getting cheaper to run. Reuters noted the hotter price readings are strengthening expectations that the Federal Reserve will stay on hold this year, while economists quoted in the consumer survey said higher diesel costs will bite hardest for low- and middle-income households. If fuel stays expensive and businesses keep passing along transport and input costs, the squeeze will show up first in margins, then in spending, and finally in the goods sitting on shelves.